For junior Ryan Padgham, it’s groceries. For his mom, Pat Rogan, it’s travel. For his grandfather, John Rogan, it’s home.

What we spend our money on says a lot about what is important to us, but everywhere we look, we are assaulted with stereotypes. These are molds we’re supposed to fit into based on our age, experience and status — molds that tell us what we’re supposed to value and how we should get it.

Things like groceries, vacations and homes are simply tangible manifestations of underlying values, the raw reasons for how we think about, talk about and most importantly, spend our money.

***

Padgham, a business major, invests in stock and can carry on a conversation about mutual funds and cash outflows. He calls his Welch’s fruit snacks a luxury item.

Ask him what he spends his money on, and he’ll tell you that he’s living out the poor college student cliché just like everyone else at IU.

“Groceries take up a very large part of the money I earn,” he said. “So my luxury item purchases have fallen drastically.”

When it comes to spending money, Padgham has a system in place: debit card for necessities like groceries and cash for extra expenses like going out to dinner.

“If I don’t have enough cash, I generally don’t go out to eat,” he said. “It’s kind of like my own little security.”

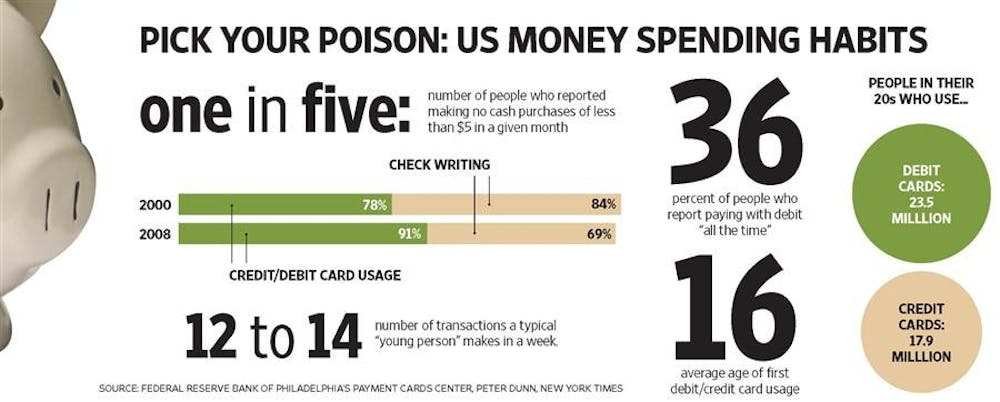

According to a study conducted last fall by Experian Simmons Research, a market research group in Fort Lauderdale, Fla., almost 70 percent — or 23.5 million — of 20-somethings have a debit card, and 53 percent — or 17.9 million — have a credit card, according to a New York Times article.

However, this increase in debit card use among young people may only be a short-term result of the introduction of debit cards as a mainstream payment option.

As today’s college students get older and reach an age where credit card use is historically high, it is likely their dependence on debit cards will transform into credit card usage, according to a May 2010 report by the Federal Reserve Bank of Philadelphia’s Payment Cards Center.

Padgham works as a waiter at Fortune Cookies. He is one of the few young consumers who still deals in cash on a regular basis.

By swiping his debit card for larger purchases, he can mitigate the remorse of handing over a chunk of change while still keeping track of his spending. At the same time, he doesn’t have to keep track of his more frivolous spending habits because they’re all in cash. When the cash is gone, he’s done.

“The more times you hand over a debit card, the less you care about how much something costs,” said Peter Dunn, founder of Green Candy, an Indianapolis-based personal finance website geared toward college students and recent graduates. “That physical action of moving the debit card toward the counter feels the same whether it’s $10 or $100.”

Since using a plastic card is psychologically different from writing a check or counting cash, it can often lead to more frequent use as well.

Dunn said the average young person spends money 12 to 14 times a week, which is more often than people did 20 years ago.

Padgham said he does his best to mitigate this not only through his use of cash, but also by not having a credit card.

“I hate debt,” he said. “One thing I hate more than anything else is owing people money, so I’ve always been weird about getting a credit card ... I’ll earn my money and then spend it as I have it. That way I monitor how much I’m spending based on what I’m earning, not any type of borrowed funds.”

***

When it comes to money, cautious is how you would describe Padgham’s mom, executive associate dean of the School of Education at IU-Purdue University Indianapolis. Pat shares her son’s aversion to debt and doesn’t feel comfortable carrying cash. She limits the number of payment methods she uses to credit and check so she can better monitor them.

Regardless of the reasoning — security or ease of using plastic — many people, like Pat, are moving away from cash.

According to the May 2010 report by the Federal Reserve Bank of Philadelphia’s Payment Cards Center, in 2008, 91 percent of people reported using plastic in a given month, up from 78 percent in 2000. The same report found that cash use was also down.

In fact, one in five consumers reported making no purchases of $5 or more with cash in a given month.

A Visa Payment Panel Study conducted during the past 20 years found that consumers today exhibit a more defined usage preference in their spending and are better able to articulate their reasoning for using one form of payment instead of another.

Although Pat uses her credit card most frequently, she said every time she does it’s a conscious decision.

“I think ‘should I pay cash, or should I write a check or should I pay by credit card?’ I am thinking ‘well, whatever goes on the credit card then I’m going to need to be paying off,’” she said. “I don’t want that amount to get higher than what I can pay off. So I am contentious.”

“Writing a check will suffice a lot of times, you know, just to come straight out of the account so I don’t have to put it on a credit card that’s earning interest,” she said.

For Pat, growing up in an army family with eight siblings was a lesson in how thin money could be spread.

Weekly trips to the grocery store warranted two carts and countless gallons of milk. Pat, the fourth oldest, learned to eat, shower and do chores on a schedule and wore a hand-me-down wardrobe.

With two children of her own, Pat still practices the frugality that her mother taught her. But another aspect of her childhood has come into play in determining how she spends her money.

“My upbringing as an army brat was on the go,” Pat said. “We moved every three or four years, so that was probably instilled in me in terms of that comfort of being out and about in other countries and traveling. That was a lifestyle, a personal value I wanted to share with the kids.”

So, in exchange for living sensibly and not indulging deeply into material things, Pat and her husband have been able to make an investment in experiences for their children — trips around the world, from Wisconsin and the Caribbean to London and Barcelona.

“My husband and I value traveling and seeking new and different experiences for ourselves and our children, so we like to spend our money on trips and events,” she said.

***

It’s easy to classify John Rogan as old-fashioned. He grew up during the Great Depression. He introduces himself as Colonel Jack and spent 25 years in the military, frequently moving his wife and nine children across the world. He’s lived in the same house for 40 years.

Having a place to call home — a house, a town, a church, a place for his family to come back to — is what John is willing to spend his money to perpetuate.

“Finally settling down in Middleton, Wisconsin, meant a lot,” he said. “It really represents our first home as opposed to all those other homes that we lived in temporarily. It means a lot to our children, even though they don’t live here. They look forward to coming home.”

After the United States dropped the atomic bombs on Japan, John became a finance officer for the military, eventually getting his MBA from the Kelley School of Business.

Having a background in finance, John has come to embrace new technologies such as online bill payments and debit cards. These methods are certainly practical, but John said they also require extra vigilance.

“I keep a substantial amount of money in my checking account, so I don’t have to worry about it. On the other hand, I have to be very careful with how I handle the debit card so it doesn’t get into the wrong hands,” he said.

Regardless of how John spends his money, what he does or doesn’t spend it on is telling.

With his house paid off and a used 2003 Toyota Camry sitting in his garage, John certainly lives a comfortable life — one he said is the result of continued frugality.?“You’re not going to get to be a millionaire when you make the military a career,” he said.

Aside from their yearly trip to California, John and his wife don’t do a lot of traveling.

“I was in the military for 25 years, and I traveled all over the world,” he said. “We’ve seen just about everything that’s worth seeing.”

Dunn said the Padgham family’s transition in spending behavior is typical.

“Our grandparents ... grew up in tougher financial times, so they were trying to give our parents the childhood that they never had, and then our parents did the same for us, so the whole mentality of entitlement has really grown,” Dunn said. “I think our generation feels more entitled than our parents did when they were our age.”

What's in the bank?

Get stories like this in your inbox

Subscribe